Insight

June 2026 arrives as a month of paradox: the geopolitical shock that has defined 2026 is finally moving toward resolution, yet the very process of resolution has triggered a new set of market headwinds. The June 14th US-Iran Memorandum of Understanding, formally signed on June 17th in Geneva, marks the most significant diplomatic breakthrough since the conflict began in February. Oil has returned to pre-war levels. The Strait of Hormuz is progressively reopening. And yet equity markets have struggled, gold has fallen sharply, and the Federal Reserve under its new Chair has surprised markets with an unexpectedly restrictive policy stance.

This creates a counter-intuitive environment. Peace is deflationary for energy but that same disinflation removes the argument for rate cuts. A firmer-for-longer Fed in a post-conflict softening is not the relief rally many anticipated. For Swiss-based investors and the clients of AIX Group AG, this report focuses on what the post-war transition means for European and global portfolios, the specific implications for Switzerland’s unique macro position and the strategic framework that should guide allocation decisions through H2 2026.

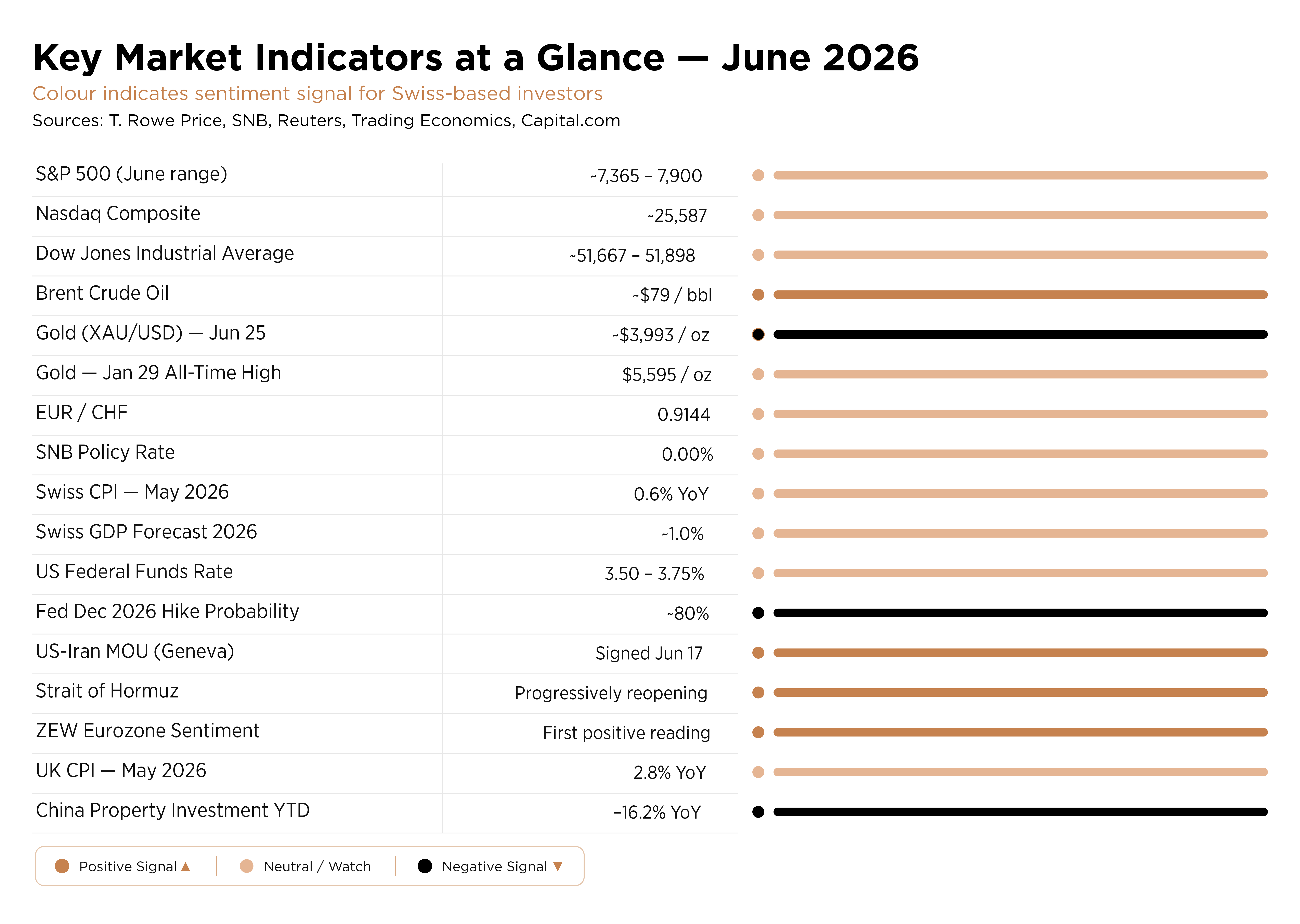

Key Market Indicators at a Glance – June 2026

The US-Iran MOU: A Turning Point But Not a Resolution

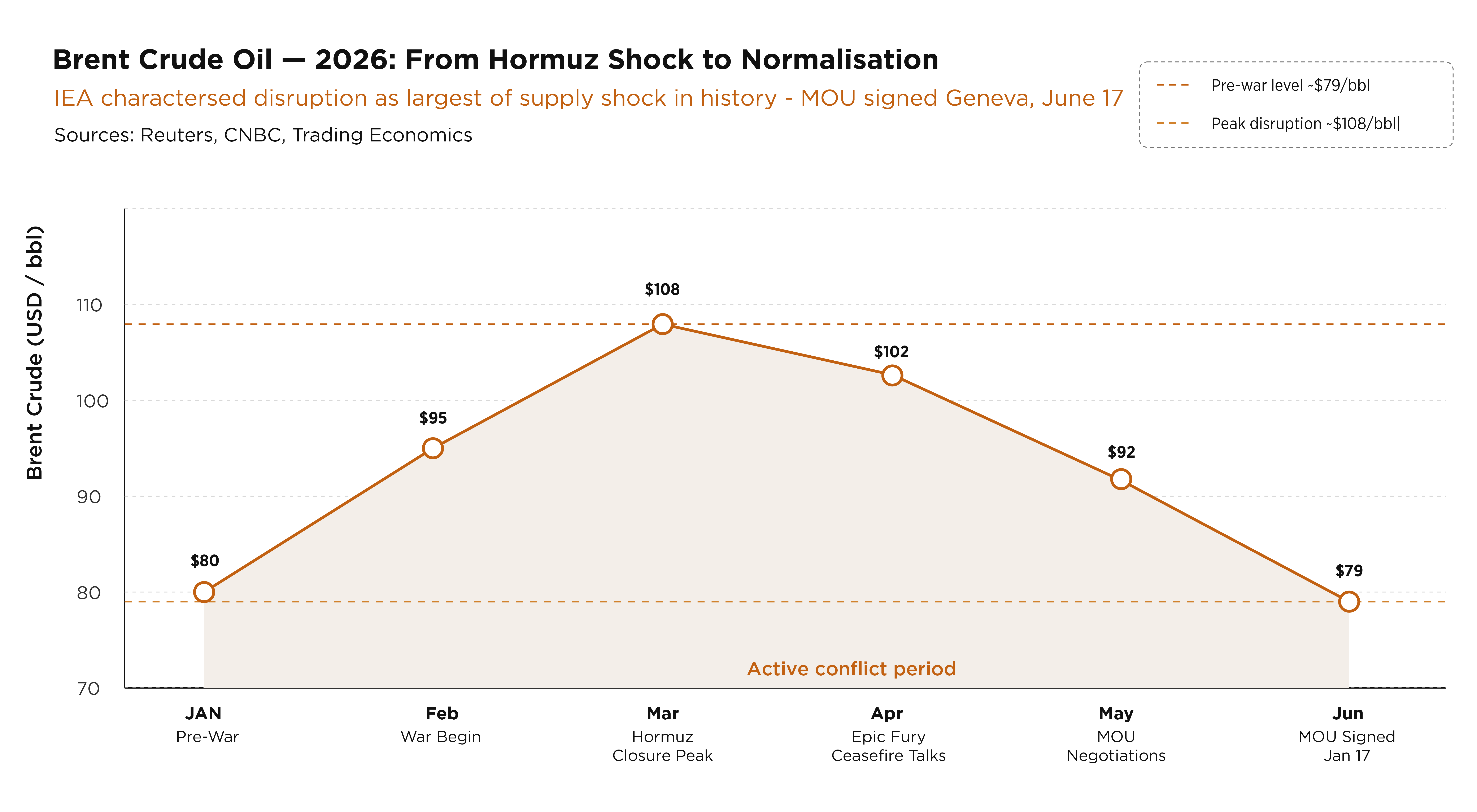

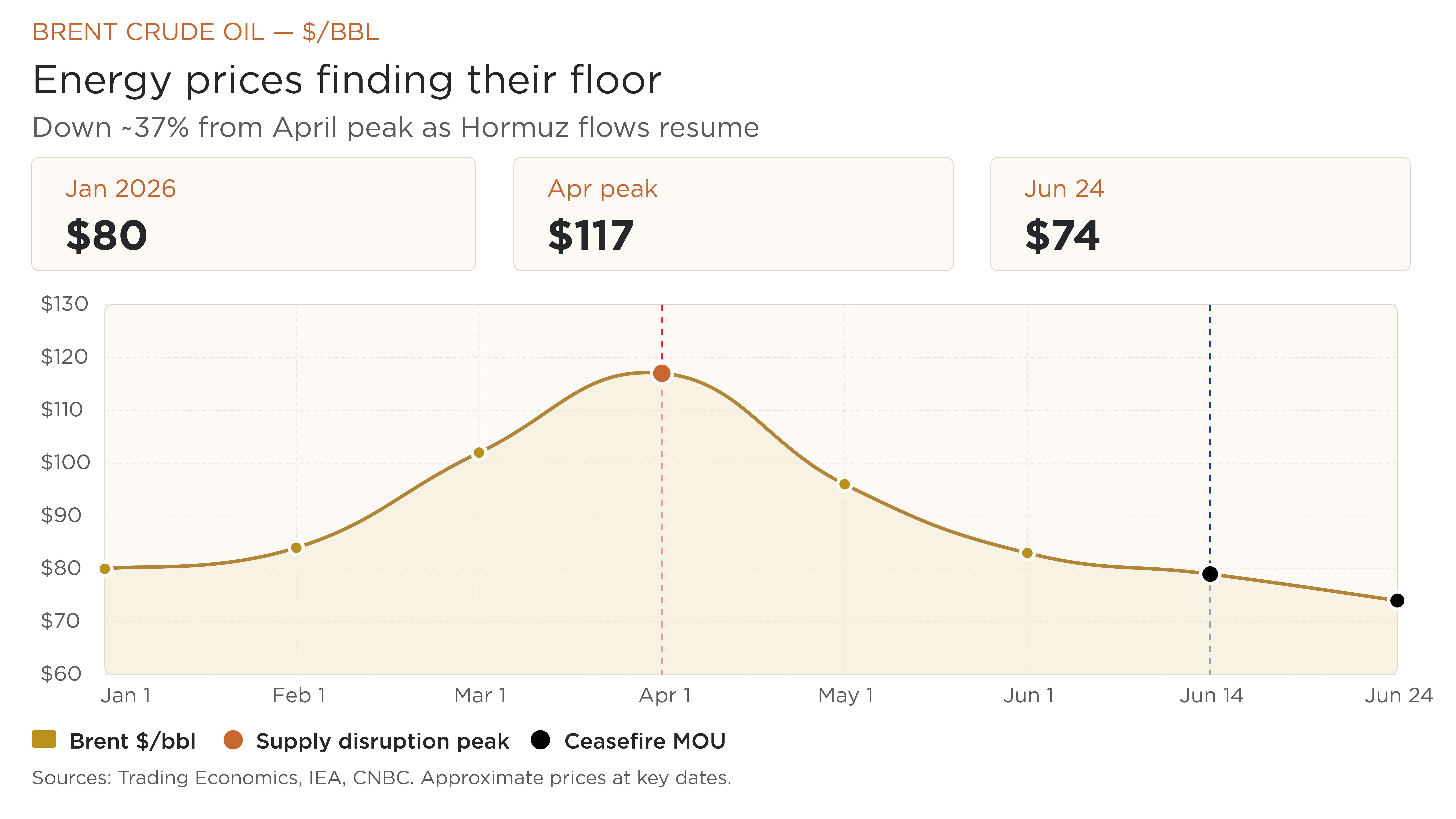

June’s defining macro event was the formalisation of the US-Iran Memorandum of Understanding on June 17th in Geneva. After more than 100 days of conflict, mediators from Qatar, Pakistan, and Oman helped broker a 14-point framework that includes a ceasefire, a 60-day negotiation window on Iran’s nuclear programme, the progressive reopening of the Strait of Hormuz and a lifting of the US naval blockade.

The market had anticipated this. Oil prices had already retreated nearly 20% from their 2026 peaks through May, and by late June Brent crude has returned to pre-war levels of approximately $79/bbl. The IEA characterised the original disruption as the largest oil supply shock in history, with output cut by over 10 million barrels per day at the peak.

The MOU is a framework, not a treaty. Key ambiguities persist:

The structural lesson here is one that prior geopolitical-shock episodes have repeatedly demonstrated: a ceasefire pauses headlines; it does not restore trust in a chokepoint. The Strait of Hormuz has been repriced as an active vulnerability rather than a background assumption. Shipping confidence will take quarters, not weeks, to fully normalise.

Global Equity and Bond Markets: Post-War, Pre-Clarity

Equity markets in June entered a mode best described as post-war uncertainty. The narrative has shifted from geopolitical fear to policy confusion. Two forces are pulling in opposite directions: the Iran peace deal and falling oil prices reduce headline inflation (typically bullish for equities and bonds); but the Federal Reserve under new Chair Kevin Warsh delivered a restrictive-leaning surprise, with the June 18 dot plot showing 9 of 18 FOMC officials favouring at least one rate hike in 2026, a meaningful shift from March projections which had pointed to cuts.

United States

US equities experienced a tech-driven correction in the week of June 16-22. The S&P 500 fell 1.44% on June 17 to approximately 7,365, with the Nasdaq shedding 2.21%. The driver was a global semiconductor sell-off, followed by pressure on mega-cap technology names. Apple fell 6.1% after raising prices citing higher component costs; Nvidia, Microsoft, Amazon, and Meta all posted losses. Defensive sectors outperformed consumer staples climbed 1.7%. This sector rotation echoes a familiar pattern of crowded momentum trades in mega-cap technology unwinding rapidly when sentiment shifts.

Markets are now pricing an 80% probability of a Fed rate hike by December 2026 and 63% for September. PCE data released on June 25 came in broadly in line, providing some relief but the tighter policy stance constrains the traditional post-shock recovery playbook.

Europe

European equities faced parallel headwinds, with the STOXX Europe 600 declining 0.57% during the mid-June tech sell-off. Germany’s DAX fell 0.8%, France’s CAC 40 shed 0.7%, the UK’s FTSE 100 closed near flat. ZEW Eurozone Sentiment posted its first positive reading since the war began — a meaningful medium-term inflection. The Bank of England held at 3.75%; UK CPI remained at 2.8% in May.

Asia and Emerging Markets

China continued to face structural headwinds. Property investment fell 16.2% year-over-year in the first five months of 2026 and the iShares China Large-Cap ETF touched a new 52-week low in mid-June, down approximately 22% from its year high. South Korean and Taiwanese equity ETFs also fell sharply amid the semiconductor sell-off.

Gold – Safe Haven Peaks

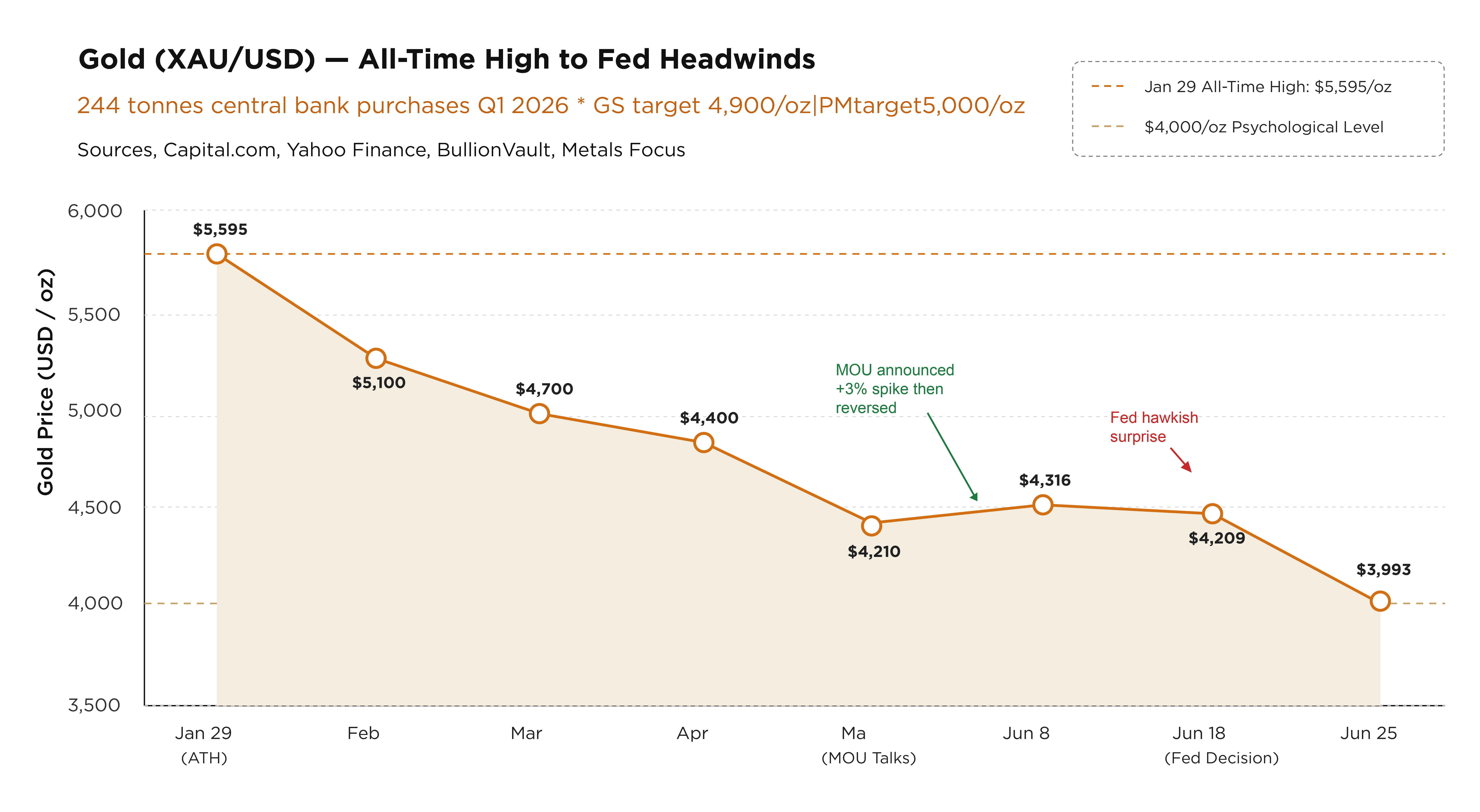

Gold’s June trajectory tells the story of 2026 in miniature. The metal hit an all-time high of $5,595/oz on January 29th, driven by central bank accumulation, geopolitical risk, and fears of Fed independence under the Warsh nomination. The peace deal announcement on June 14-15 initially sent gold up over 3%. But the subsequent Fed tightening rhetoric at the June 18 meeting more than offset those gains. By June 25, gold fell below $4,000/oz for the first time since November 2025, with futures touching approximately $3,993.

Gold in mid-2026 is caught between two structural forces:

For Swiss-based investors, the gold picture is further complicated by the CHF’s own safe-haven status. As geopolitical risk recedes, the franc may face mild depreciation pressure reducing the CHF-denominated return on gold positions and requiring careful currency hedging consideration.

Switzerland’s Resilient Outlier

Switzerland enters H2 2026 as one of the most resilient developed economies globally but resilience does not mean immunity. The SNB held its policy rate at 0.00% at its June 18 meeting. GDP growth is forecast at approximately 1.0% for 2026, improving to 1.5% in 2027. Inflation rose to 0.6% in May (from 0.1% in February), driven primarily by imported energy within the SNB’s 0-2% price stability range. The EUR/CHF rate of 0.9144 confirms the franc’s structural strength below parity, a double-edged position: strong CHF dampens import costs and inflation, but compresses returns on unhedged international assets.

Swiss real estate funds demonstrated defensive characteristics during the March 2026 correction. The SWIIT Index corrected just 5.3% versus the SMI’s 8.8%, then staged a full recovery to a new all-time high by April 14th. Vulnerabilities include exposure to US tariff policy, Germany’s industrial weakness and political uncertainty from the June 14th population referendum early indications suggest the restrictive measure failed, a meaningful positive for Switzerland’s long-term economic trajectory.

Strategic Framework for H2 2026

The transition from a war-driven macro environment to post-war normalisation is rarely as clean as markets expect. Prior geopolitical-shock cycles caution against assuming de-escalation equals a simple risk-on signal. The June data confirms that view. The geopolitical premium in oil is dissipating; the inflationary premium in rate expectations is not.

Five Positioning Principles for Swiss-Based Investors

1. Preserve Jurisdictional Advantage

Switzerland’s regulatory stability, legal predictability and monetary discipline are structural advantages most valuable in environments of global fragmentation. Jurisdictional quality is a quantifiable risk reduction in a world where capital controls, sudden tax changes and regulatory shifts have materialized across multiple regions in 2026.

2. Income is the New Growth

In a world where the Fed may hike into year-end and the SNB holds at zero, income-generating assets carry a premium. Fixed-rate bonds, private credit and real-estate income strategies all provide returns that do not depend on multiple expansion or equity sentiment.

3. Maintain Liquidity as Strategic Capital

Investors who maintained liquidity through the conflict have the flexibility to deploy at more rational valuations in H2 2026. The semiconductor-driven correction of mid-June is a preview: volatility-driven drawdowns in quality assets create entry points unavailable to fully invested portfolios.

4. Global Diversification Beyond US Beta

The structural risk of over-concentration in US large-cap equity has been a recurring theme across 2026, and that risk has materialised in June. From a Swiss base, European equities at lower valuations and with improving ZEW sentiment represent a more balanced risk/return proposition.

5. Selective Accumulation in Structural Themes

AI infrastructure capex remains a multi-year structural trend, the semiconductor sell-off in June is a positioning event, not a reversal of the underlying investment cycle. Companies in power infrastructure, data centre supply chains and energy transition are beneficiaries of sustained capital spending regardless of near-term equity volatility.

What to Watch in July-August 2026

The two highest-conviction risks for H2 2026 are the US Federal Reserve’s rate path and China’s economic stress both high likelihood and high severity in the current environment. The Iran MOU implementation, technology sector volatility, CHF appreciation risk and eurozone stagflation risk all sit in the medium category, requiring active positioning awareness rather than reactive management.

For Swiss-based investors: the Fed risk translates directly into USD strength and gold headwinds; the China risk compounds through reduced global demand for European and Swiss exports; the CHF risk demands hedging discipline on international allocations; and the tech sector risk rewards selectivity within the AI structural theme rather than passive index exposure.

Final Thought

2026 has repeatedly posed the question of whether the world was FAFO or TACO – whether geopolitical risks would materialise into structural economic consequences, or whether markets would once again fade the fear and buy the relief. The answer in June is nuanced: FAFO was real (the largest oil supply shock in history, a genuine chokepoint crisis, a war that re-priced global risk infrastructure), but the resolution is also real, and it is unfolding.

What this month reinforces is that the post-war environment is not simpler than the war environment – it is differently complex. The geopolitical premium in oil is dissipating. The inflationary premium in rate expectations is not. The Fed is tightening. The SNB is holding. And equity markets, having priced in de-escalation faster than energy systems could physically normalise, are now adjusting to a world where the recovery is real but not unlimited.

For Swiss-based investors and AIX Group AG clients, the second half of 2026 rewards disciplined positioning: structural diversification, income over speculation, liquidity as optionality, and quality over consensus. This inaugural report launches a dedicated monthly market analysis series for AIX Group AG, reflecting a broader truth about the current environment: jurisdictional strength, institutional stability, and long-term orientation are not merely preferences they are competitive advantages.

Commentary by AIX Group AG

Disclaimer

The above market analysis/information is produced for information and knowledge purposes only under personal capacity, and does not constitute any liability or obligation upon the readers or the firm to take investment decisions. Professional investors only.

References

Please select “AGREE & CONTINUE” below: By clicking the “AGREE & CONTINUE” button below, you warrant that you acknowledge that you have read and understood the Terms and Conditions and Terms of Use and agree to be bound by their terms.